In 2024, the approval of a spot BTC ETF will make this asset class more accessible to investors, with the smart contract platform, DeFi and computing token industries set to perform best.

Original title: “Crypto Market Outlook 2024: ETFs Offer Tailwinds for Other Digital Assets”

Written by Todd Groth, CFA

Compiled by: Yvonne, Mars Finance

Looking back, 2023 will undoubtedly be a year of transition for emerging asset classes. The positioning, leverage, and speculative excesses of the previous market cycle in 2022 are cleared away, creating conditions for the seeds of a new cycle to germinate in 2023. What persists and remains is a market of increased interoperability between protocols and projects, with builders and market participants catering to regulated institutional investors with an eye toward greater real-world utility.

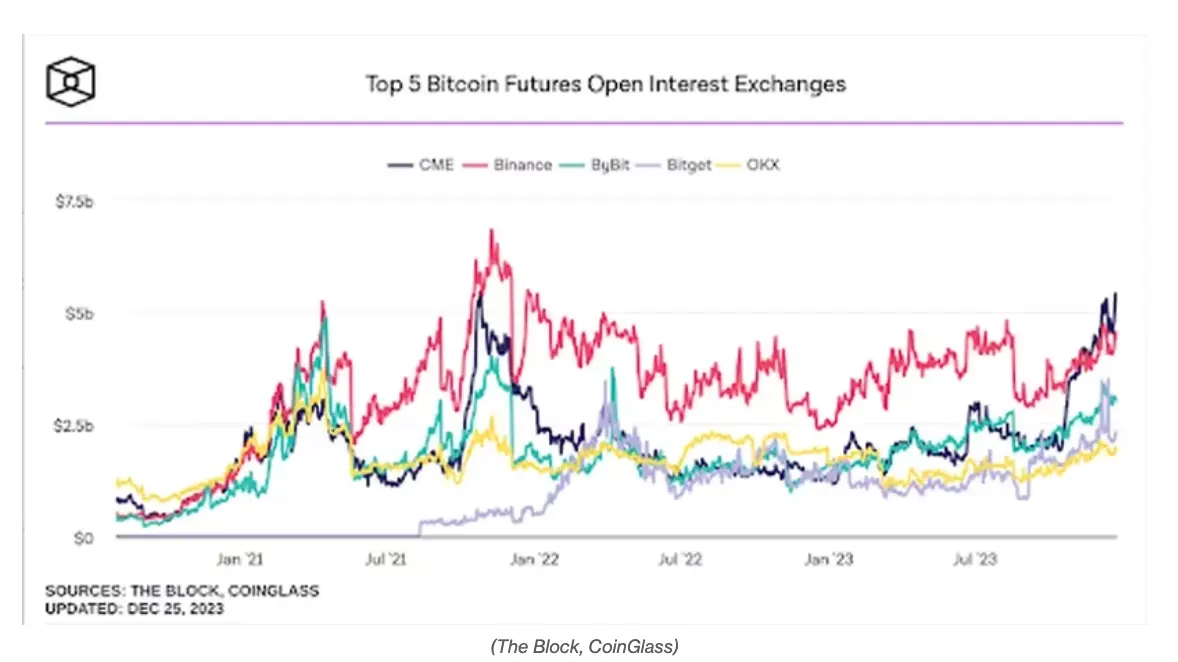

Leadership at once-prominent cryptocurrency exchanges like FTX and Binance has changed, with more regulated players like Coinbase, Bullish (now the owner of CoinDesk), and EDX leading the market. At the same time, the trading volume of BTC and Ethereum futures contracts on traditional futures exchanges such as CME is also growing (see chart below), and its number of BTC futures open contracts has exceeded Binance.

We also witnessed yet another effort to list a spot token ETF in the United States, with BlackRock surprising the market by filing an application with the SEC in June. This encouraging institutional development helps support demand for BTC as a real asset and as a hedge against currency devaluation against a financial system flooded with fiat liquidity and supportive stimulus, reinforcing the case for wider adoption of the digital asset .

The macroeconomic relevance of digital assets has also decreased during 2023. Cryptocurrencies largely decoupled from U.S. stocks and gold during the year (see rolling correlation chart above), although the levels of volatility achieved were lower than in previous years. Surprisingly, the volatility of ETH in 2023 is almost the same as that of BTC, breaking the historical norm of BTC volatility being generally about 20% higher. BTC’s volatility has dropped to a level similar to the volatility of a single stock, which is consistent with traditional Asset classes are more consistent.

Collectively, these developments mark the maturity of the cryptocurrency market and the ongoing transition to an institutional landscape. This transition and the expansion of the ecosystem to more traditional and regulated market participants is expected to be central to the next market cycle.

Outlook 2024

We expect that 2024 will see the crypto market further mature for institutional investors. This institutionalization is consistent with the strong performance of BTC and ETH, even at the end of the U.S. rate hike cycle, and is decoupled from short-term macro risk factors, suggesting that BTC and ETH are increasingly viewed as similar to gold and oil. Unique physical assets. We anticipate that these characteristics will drive demand for BTC and ETH as liquid alternatives and diversifiers to traditional bonds, and help asset allocators reinvigorate their traditional stocks/bonds with a novel source of price appreciation portfolio.

We expect the spot BTC ETF to be launched in the first quarter of 2024. While this is a consensus, we believe that the approval of a BTC ETF is unlikely to become a typical “buy the rumor, sell the news” event in the medium to long term, as it allows capital to enter through familiar and regulated exchange-traded products. this asset class.

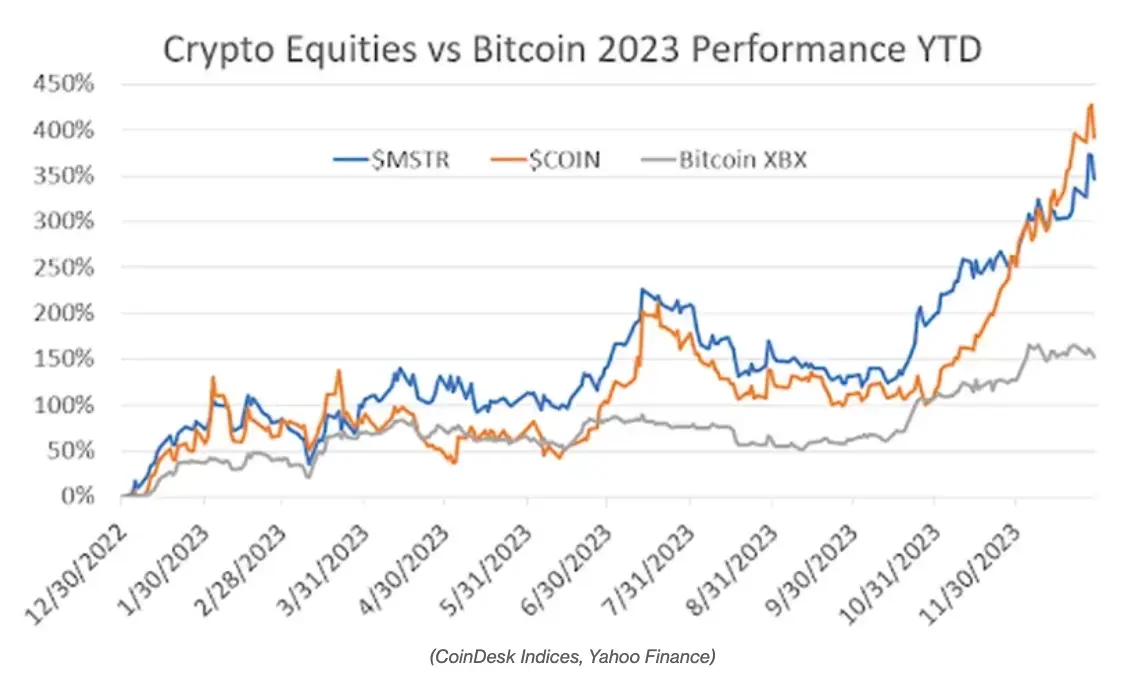

If anyone doubts the pent-up demand for these assets in more traditional, regulated packaging, look at the performance of Coinbase and MicroStrategy stocks in 2023, both of which have outperformed BTC over this period Many (see picture below).

These newly launched ETFs will make this asset class more accessible to a wider range of investors, including registered investment advisers (RIAs), pension funds and hedge funds, and enable investment banking structuring teams to build new products on top of ETF vehicles .

We believe the inflows into these ETFs will create long-term tailwinds for the market that have not yet been fully appreciated. Assets under management currently managed by RIAs are estimated to hover around $128 trillion in 2022 (Source: Association of Investment Advisers 2022 Outlook), assuming a 1-2% portfolio allocation to digital assets through spot ETF products. Will bring an additional $1 to $2.5 trillion in new capital to the crypto ecosystem. It’s worth noting, however, that potential capital inflows into the market via ETFs will be limited to BTC and ETH, which may further differentiate them from smaller digital assets, known as “altcoins.” Nonetheless, we do believe that the appreciation of these two mega-coins will be distributed across the broader ecosystem to smaller protocols, as they are the primary store of value for crypto-native investors.

If the U.S. economy slips into recession in the second half of 2024 due to the lagged effects of an accelerating interest rate hike cycle, and interest rates are subsequently lowered, we expect digital assets to benefit broadly from the expected and expected stimulus. The digital scarcity of BTC, which has experienced its “halving” in 2024, will become increasingly attractive in an environment of further increases in federal deficits and spending. Ethereum’s merged token economy is also becoming increasingly deflationary, which further enhances ETH’s appeal in this potential scenario.

Against this macroeconomic backdrop, we expect the smart contract platforms, decentralized finance (DeFi) and computing token industries to perform best in 2024, as all three industries benefit from on-chain as they interact with each other Increased activity:

- Smart contract platform activities require the use of its native token for blockchain transactions

- DeFi tokens benefit from trading volume and lending transaction fees

- Price oracle tokens in the computing space (such as Chainlink) provide the price data needed by the entire blockchain ecosystem to facilitate transactions

The computing space also contains protocols and projects focused on decentralized computing and artificial intelligence topics, which are further supported by ChatGPT, AI-driven narrative, which positions this space to outperform all others in 2023 , we should expect this to be a pillar of continued support for the sector in 2024. For more information on the cryptocurrency industry definition, click here.

While recessions and interest rate cuts can be a favorable macroeconomic environment for digital assets, it can also be affected by periods of low liquidity and deleveraging. Therefore, we believe that position sizing and portfolio construction will be more important than judging market direction in 2024 and recommend that readers use CoinDesk’s BTC and ETH Trend Indicators (BTI and ETI, respectively) when considering allocation decisions to the asset class. . For more information about BTI and ETI, please click here.

When investing in digital assets, investors should also consider their risk tolerance and time investment. For those looking for more passive investments, major coins such as BTC and ETH may be safer options in their intended and regulated ETF wrappers. On the basis of ETH positions, you can also obtain additional income through marking. Our comprehensive ETH marking rate (CESR) provides an annualized marking rate and a benchmark marking index. For more information about CESR, click here.

For those investors looking to passively invest in smaller tokens and protocols with greater growth potential, we recommend broadly diversified indices with limits on Bitcoin and Ethereum exposure to manage idiosyncratic token risk while investing in altcoins. Coin tilt as altcoins tend to benefit from the mid to late stages of cryptocurrency bull markets.

In short, we have emerged from the cryptocurrency winter, and our ecosystem is stronger, more supportive, and has a broader narrative than the previous cycle and should be able to support the new market cycle until 2024.