Analyze the development trends of the DeFi ecosystem and discuss the challenges and opportunities faced by projects in the changing market.

Written by: Jiang Haibo, PANews

DeFi has experienced rapid growth and evolution over the past few years. From the initial experimental project, it has now become an indispensable cornerstone in the Crypto field. Many projects such as Uniswap, Curve, Aave, and Compoud have stood out in this process, but the competition in this track is also becoming increasingly fierce. For example, DEX continues to reduce handling fees to attract transaction volume, and lending protocols increase the loan-to-value ratio to improve capital efficiency. Projects are also actively developing new products to seize more markets. What trends might DeFi exhibit in 2024? PANews shares the following key trends and predictions in the DeFi field.

Protocol platformization

As the DeFi field develops and matures, major DeFi protocols are no longer satisfied with their core businesses and hope to shift from single-function projects to platforms that provide a comprehensive package of services.

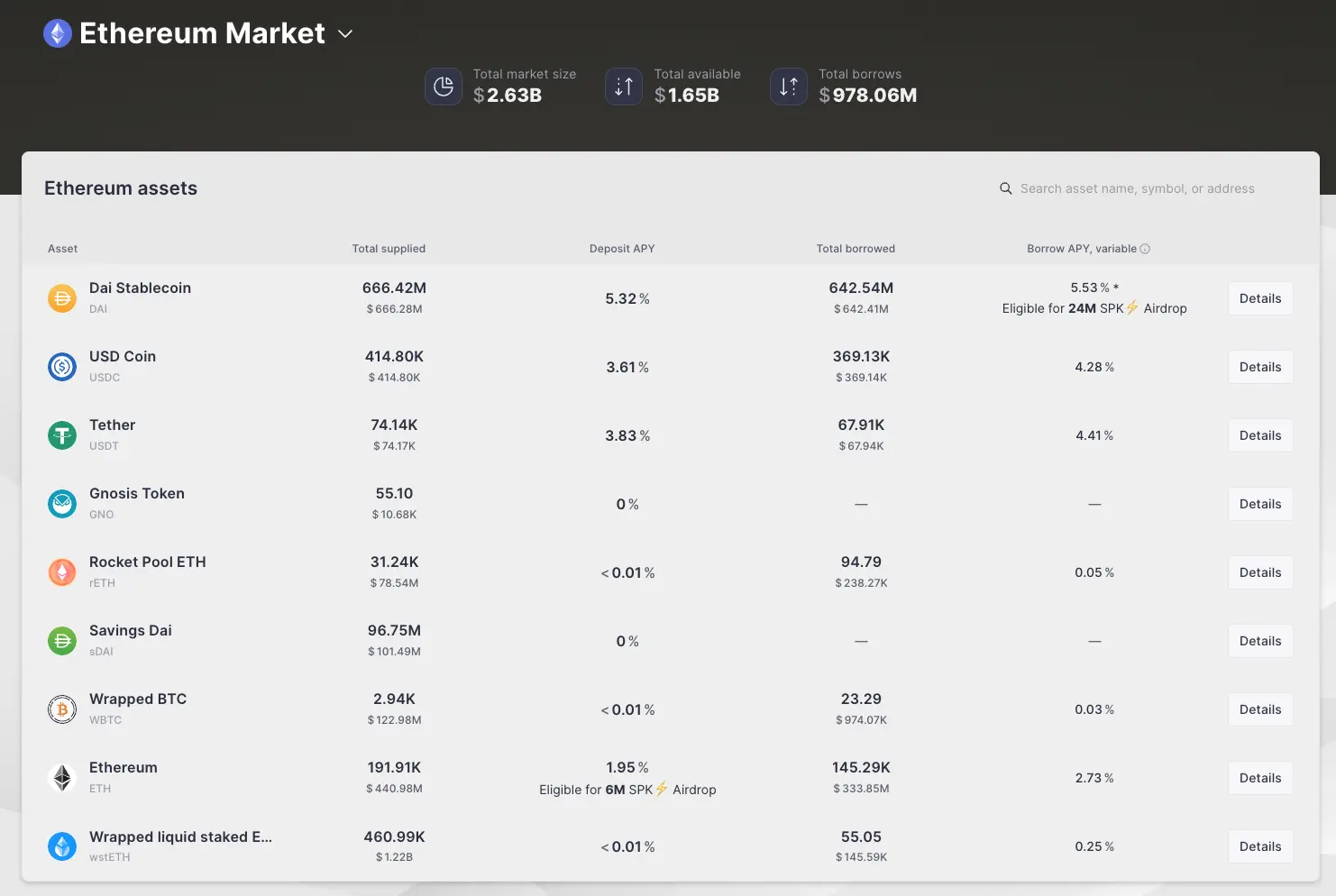

In the past year, among the DeFi protocols that everyone is familiar with, MakerDAO’s SubDAO Spark was launched. As of December 29, the TVL on Ethereum reached 1.65 billion US dollars, becoming a major lending protocol.

Curve and Aave have developed their own stablecoins crvUSD and GHO respectively. Uniswap has launched its own wallet application and previously acquired the NFT platform Genie. Thala on the new public chain Aptos has single-handedly developed stablecoins, DEX, Launchpad, and liquidity staking functions, including almost all common DeFi businesses except lending.

The platformization of DeFi protocols has become a trend, which is also a symbol of the maturity and continuous involution of DeFi. This trend is likely to continue and intensify in the future.

The leading DEX and lending protocols will continue to maintain their advantages

Leading DeFi protocols such as Uniswap, Aave, MakerDAO, etc. were all products before the last bull market. They have strengthened their position in the continuous evolution of the market, demonstrated strong network effects and brand influence, and are constantly being updated. . For a period of time, they will still occupy a major market share and will be difficult to replace.

Uniswap announced the v4 version, allowing various customized functions to be added through “hooks”; Uniswap Aave v3 improves capital efficiency and scales across multiple chains, further solidifying its position as a major lending platform in the DeFi ecosystem.

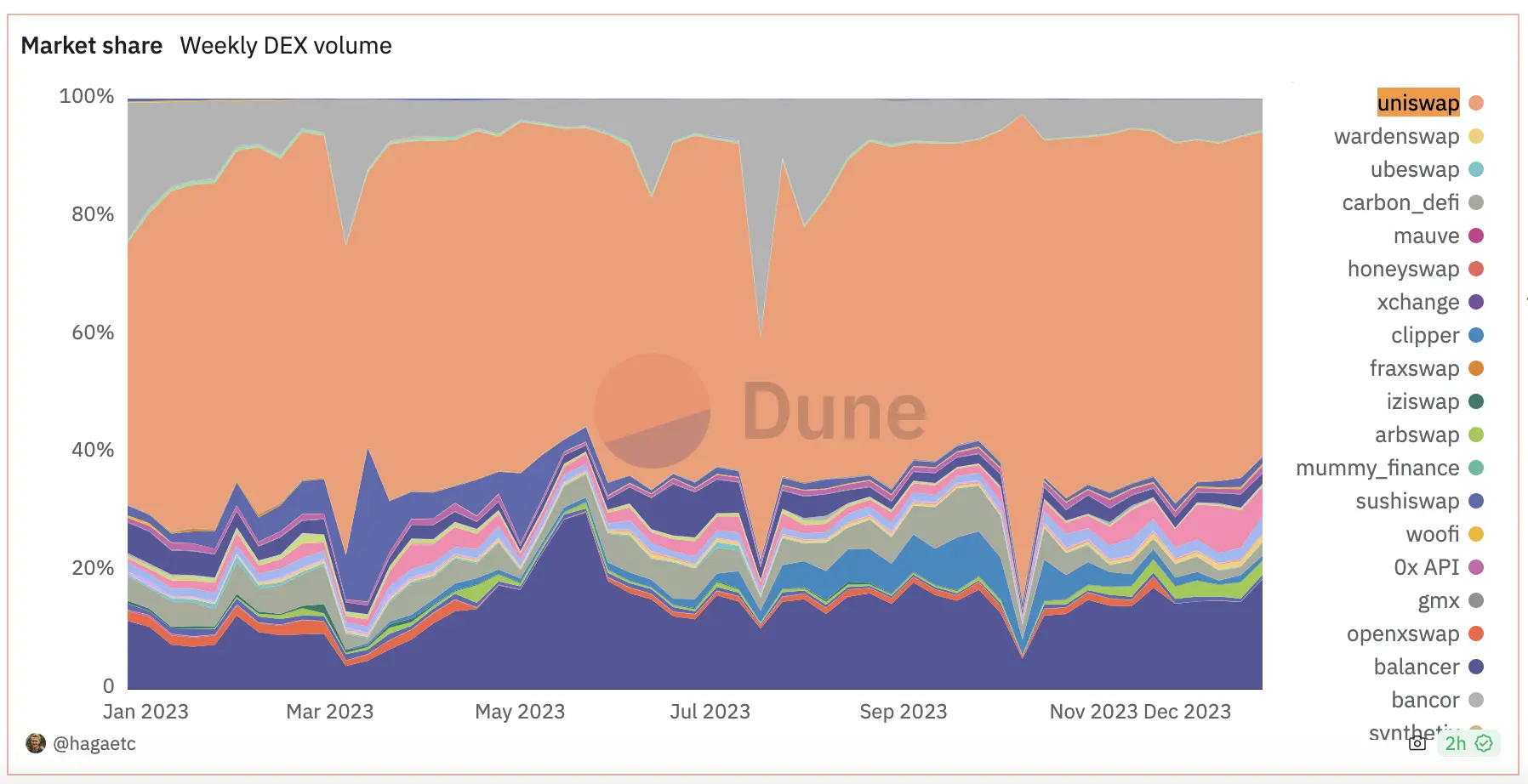

Dune co-founder hagaetc’s dashboard shows that Uniswap still holds about 55% market share among DEXs on major EVM chains.

Liquidity mining will gradually become a thing of the past, and funds will flow to more efficient places.

In public chains with mature ecosystems such as Ethereum, Solana, and BNB chains, liquidity mining has gradually become a thing of the past. Projects rely on “real returns” to attract funds, and funds are more likely to flow to more efficient places.

Recently, the price increase and ecological development of SOL in Solana have triggered FUD on Ethereum and its ecosystem. Against the backdrop of frequent MEME currency transactions, DEX on Solana has demonstrated strong capital efficiency. With current liquidity providers relying primarily on real revenue generated from transaction fees, these projects are likely to attract more funds in the short term.

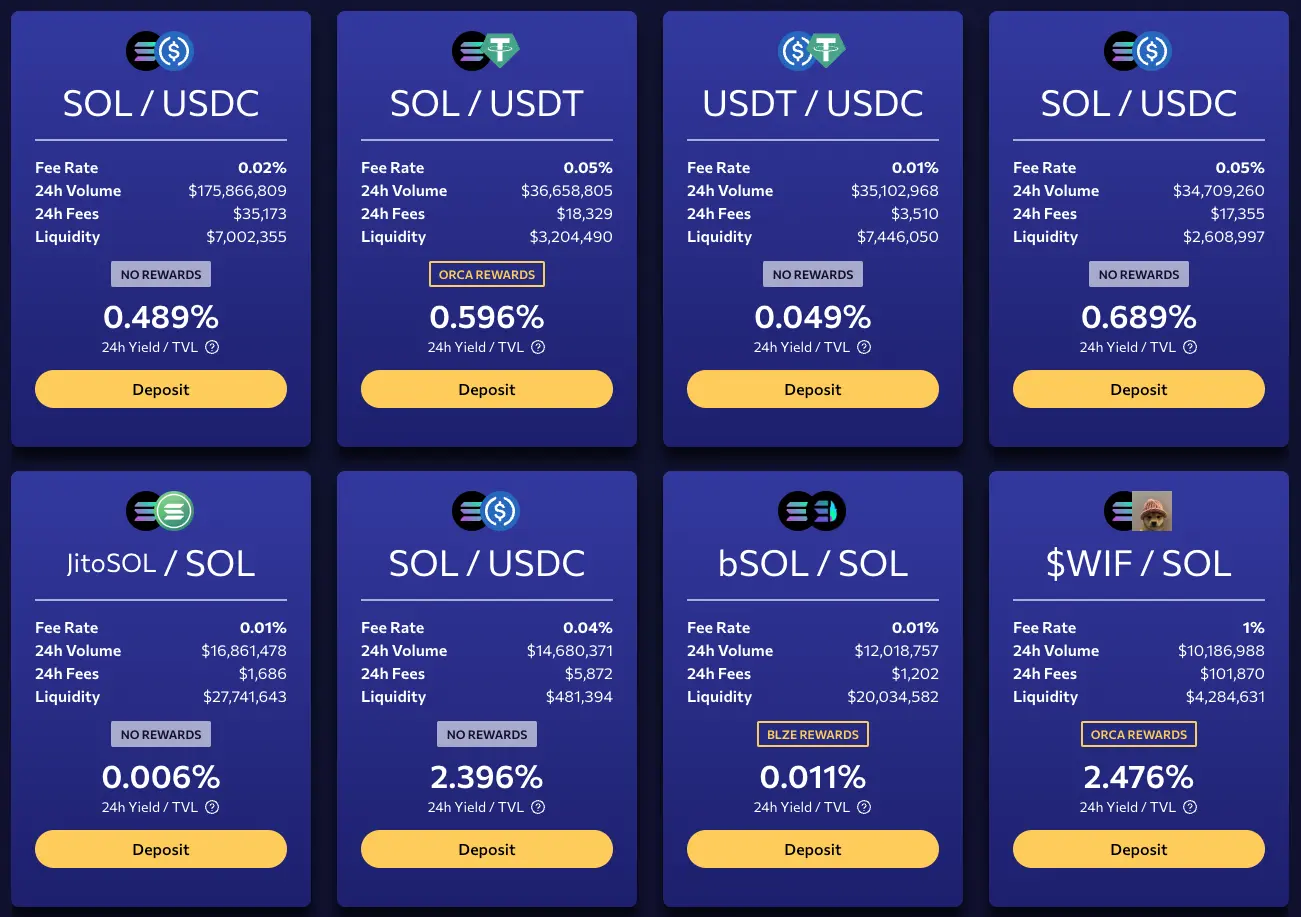

Taking the data on December 30 as an example, in the past 24 hours, the SOL/USDC and SOL/USDT pools with the most liquidity in Orca provided liquidity with average daily income from transaction fees alone, which was close to or exceeding 0.5%, and the fees The handling fee charged by the SOL/USDC pool with a fee ratio of 0.04% reached 2.396% of liquidity in a single day.

This is unimaginable on other chains. For example, on Ethereum, the top three trading pairs of ETH/stablecoin liquidity provide daily income of 0.068%, 0.077%, and 0.127% respectively.

In the case of completely unequal profitability, professional liquidity providers are more likely to move to places with stronger profitability and higher capital efficiency. This is not inconsistent with the previous point. The top DeFi projects have better fundamentals, are safer and more stable, but their growth rate is also relatively slow. Emerging projects will maintain faster growth when the storm hits, and expectations for future growth will also be reflected in token prices, but how long this growth can be sustained is a question.

LST will lead the TVL growth of new public chains

Although liquidity staking projects have already appeared on many blockchains that use proof-of-stake mechanisms, Liquidity Staking Tokens (LST) only began to be intensively discussed before the Ethereum Shanghai upgrade. Now the leader in liquidity staking, Lido, has become The project with the highest TVL, bar none.

Similarly, this trend has also appeared on Solana, with two liquidity staking projects, Marinade and Jito, occupying the top two spots in Solana ecological TVL respectively. Liquidity staking projects have also led the recent growth of Solana TVL. On the one hand, Jito’s airdrop expectations before the currency issuance have attracted the amount of pledges; on the other hand, Marinade, Jito and other liquidity staking projects have continued to encourage LST in Solana DeFi. The use in the protocol promotes the overall improvement of Solana TVL.

Other public chains that want to improve TVL seem to have discovered the secret of LST’s ecological promotion. For example, in the Sui ecosystem, the APR of the haSUI-SUI trading pair on Cetus is 49.04%, of which 48.09% comes from the SUI tokens officially rewarded by Sui. In the Avalanche ecosystem, Benqi, the leader in lending, has also developed the LST business. Currently, the TVL brought by LST has exceeded that of lending.

Perp DEX may have competitive projects

The decentralized perpetual contract exchange, namely Perp DEX, was once favored by many people and has also launched projects such as dYdX, Synthetix, and GMX. dYdX is an order book type. As for the liquidity pool types Synthetix and GMX, although it is already the main Perp DEX, they still have their own advantages and disadvantages in using them.

GMX v1 has been criticized for being unbalanced in the long-short ratio during unilateral market conditions and not friendly to liquidity providers. Both long and short positions at the same time require currency borrowing fees and a high transaction fee ratio, which is not friendly enough to traders. But its slippage-free liquidity feature is something other projects don’t have.

GMX v2 introduces transaction slippage for long-short balance. Transactions that balance long-short will be compensated, and transactions that unbalance long-short will be punished. However, when opening a position, users cannot predict whether the long and short positions will be balanced when closing the position, which brings uncertainty. Punitive transaction slippage may reach 0.8% of the position or even higher. Taking into account the leverage ratio, such as 10 times leverage and a slippage of 0.8%, a single transaction will result in a loss of 8% of the principal.

Compared with GMX v2, the funding rate in Synthetix fluctuates more. Likewise, users may suffer losses due to the increase in funding rates after opening a position. In addition, Synthetix uses Pyth’s off-chain oracle, and there is an 8-second delay between order placement and execution, so what you see is what you get.

Some recent Perp DEXs have shown attractive features, such as Drift’s DLP pool, in which BONK-PERP shows a 30-day return on providing liquidity of 2000%, and HNT-PERP has a return of 439%. Although using leverage to provide liquidity in Drift’s DLP pool is very risky and you may lose all your principal, you may also get higher returns. In addition, projects such as Aark Digital and MXY Finance provide Perp DEX solutions with higher capital efficiency.

Real World Assets

Real World Assets (RWA) are actually a controversial category of projects. First of all, it has an off-chain part, which may need to rely on a single entity and may also face supervision, which is not completely consistent with the decentralized characteristics of DeFi.

Although we believe there are better opportunities in the real world and everything can be tokenized, at this stage, U.S. debt seems to be the only direction that can be applied on a large scale. Although other real estate, artworks, etc. can also be tokenized and put on the chain, because they are non-standardized products, they are not originally liquid and still have no liquidity on the chain.

With expectations of interest rate hikes in the United States, short-term U.S. bond yields are expected to drop significantly in 2024, which will directly affect the yields of RWA products such as MakerDAO. The crypto market may enter a bull market during this period, demand for stablecoins will increase, and the appeal of such products may decrease. Judging from recent data from MakerDAO, the issuance of DAI has begun to decline since late October.

But this does not prevent Crypto entrepreneurs from exploring and being interested in this track. In this process, RWA may introduce powerful traditional financial institutions as partners, which will at least be a great narrative.