Jito, as MEV infrastructure within the Solana ecosystem, derives its importance from its role as a “revenue layer.” It captures MEV by optimizing transaction ordering and distributes that value to users through liquid staking.

Within this system, JTO does not directly generate yield. Instead, it represents control over how the system operates. For that reason, JTO is better understood as a “governance infrastructure token,” whose value depends on the growth and influence of the protocol.

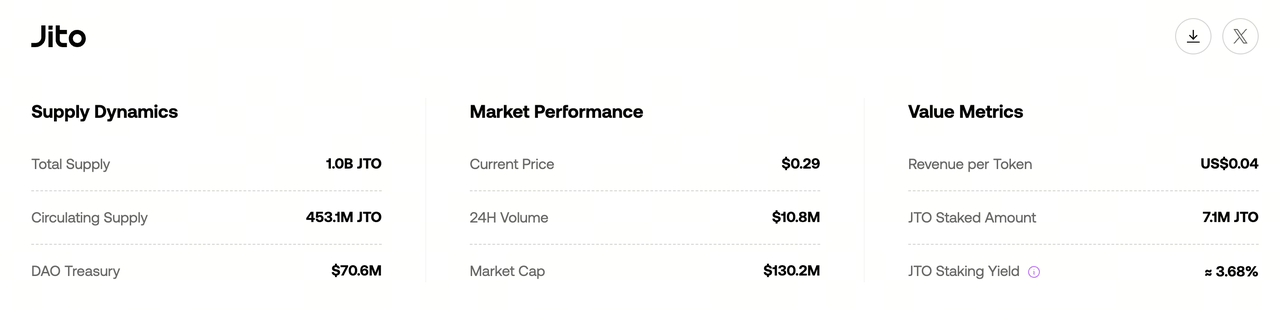

JTO Token Overview

As the native token of the Jito network, JTO has a total supply of 1 billion tokens, issued on the Solana blockchain. Its primary functions are governance and ecosystem incentives. It operates alongside Jito’s core products, such as JitoSOL, creating a complementary relationship.

Unlike many DeFi tokens, JTO does not currently offer direct revenue sharing. Instead, it indirectly influences how rewards are distributed through governance. This means its value is driven more by long-term expectations than short-term cash flow.

Source: JTO Hub

Source: JTO Hub

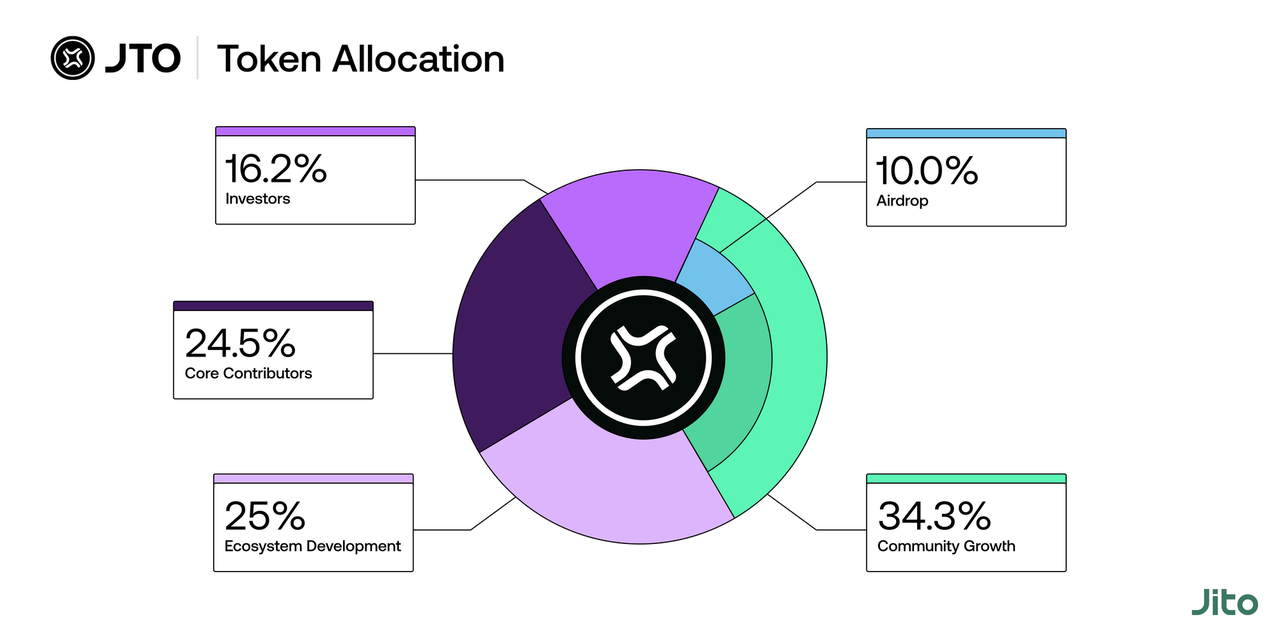

JTO Token Distribution Breakdown

The initial airdrop accounts for 10% of the total supply, broken down as follows: 80% to JitoSOL users (80 million tokens), 15% to Jito-Solana validators (15 million tokens), and 5% to MEV searchers (5 million tokens). The remaining 90% is allocated to core contributors (24.5%), investors, the DAO treasury, and ecosystem funds.

Of the airdropped tokens, 50% were unlocked at TGE (Token Generation Event), while the remaining 50% are released linearly over 12 months.

In September 2025, the Jito Foundation announced a buyback program using the Community Strategic Development fund, purchasing JTO via a TWAP mechanism to stabilize the market and strengthen DAO reserves.

Core Utilities and Use Cases of JTO

JTO is primarily used for governance voting. Holders participate in protocol decisions through the Jito DAO, including parameter adjustments such as Block Engine fees, tip distribution rules, protocol upgrades, and treasury spending.

Other use cases include staking incentives. JTO can be used to boost liquid staking rewards or serve as part of validator participation within the Jito ecosystem. In the future, it may expand into areas such as MEV searcher auction priority or discounts when converting into JitoSOL.

How JTO Captures Value: Sources and Growth Path

JTO’s value does not come directly from cash flow but is reflected indirectly through protocol growth.

Source: JTO Hub

Source: JTO Hub

First, as activity within the Solana ecosystem increases, on-chain transactions rise, leading to greater MEV extraction. This expands Jito’s revenue and strengthens its position within the ecosystem.

Second, the growth of JitoSOL’s TVL means more users are participating in its staking system. This reinforces network effects, making Jito a default choice and increasing the importance of its governance token.

In addition, participation from validators and searchers creates a positive feedback loop. More participants generate higher revenue, and higher revenue attracts even more participants.

As a result, JTO’s value growth can be understood as a “flywheel”: MEV growth → protocol revenue increase → more users and validators → ecosystem expansion → increased JTO value.

Long-Term Value Logic of JTO

Over the long term, JTO’s value depends on whether it can establish itself as the core governance layer for MEV and staking within the Solana ecosystem.

In bull market conditions, increased transaction activity leads to higher MEV revenue, which could rapidly expand Jito’s influence and drive demand for JTO.

In bear markets, declining transaction volume reduces MEV revenue, making JTO’s value more dependent on governance expectations and ecosystem development.

For this reason, JTO is better evaluated as a long-term infrastructure growth asset rather than a short-term yield instrument.

Risks and Uncertainties of JTO

Despite its growth potential, JTO carries several risks.

The first is value capture. If the protocol fails to establish a clear mechanism for distributing revenue, the token may struggle to reflect ecosystem growth.

Second, there are risks associated with MEV itself. MEV remains controversial, particularly regarding fairness and user experience, which could introduce regulatory pressure.

Competition is another key factor. Other liquid staking protocols or MEV solutions could erode Jito’s market share.

Finally, token unlock schedules may increase supply in the short term, potentially impacting price performance.

Conclusion

JTO derives its value from control over MEV revenue distribution and protocol governance. At its current stage, its valuation is driven more by expectations and ecosystem growth than by direct cash flow.

In the long run, JTO’s potential depends on two key factors: Jito’s position within the Solana ecosystem and the expansion of the MEV market.

FAQs

Does JTO provide revenue sharing?

Currently, JTO is mainly used for governance and does not directly distribute revenue.

What drives JTO’s value?

Its value primarily comes from protocol growth, the scale of MEV revenue, and demand for governance rights.

What is the difference between JTO and JitoSOL?

JTO is a governance token, while JitoSOL is a liquid staking asset used to generate yield.

Is JTO suitable for long-term holding?

This depends on whether investors are optimistic about Jito’s long-term role within the Solana ecosystem.

What is the biggest risk?

Insufficient value capture and uncertainty around MEV mechanisms remain the most critical risks.