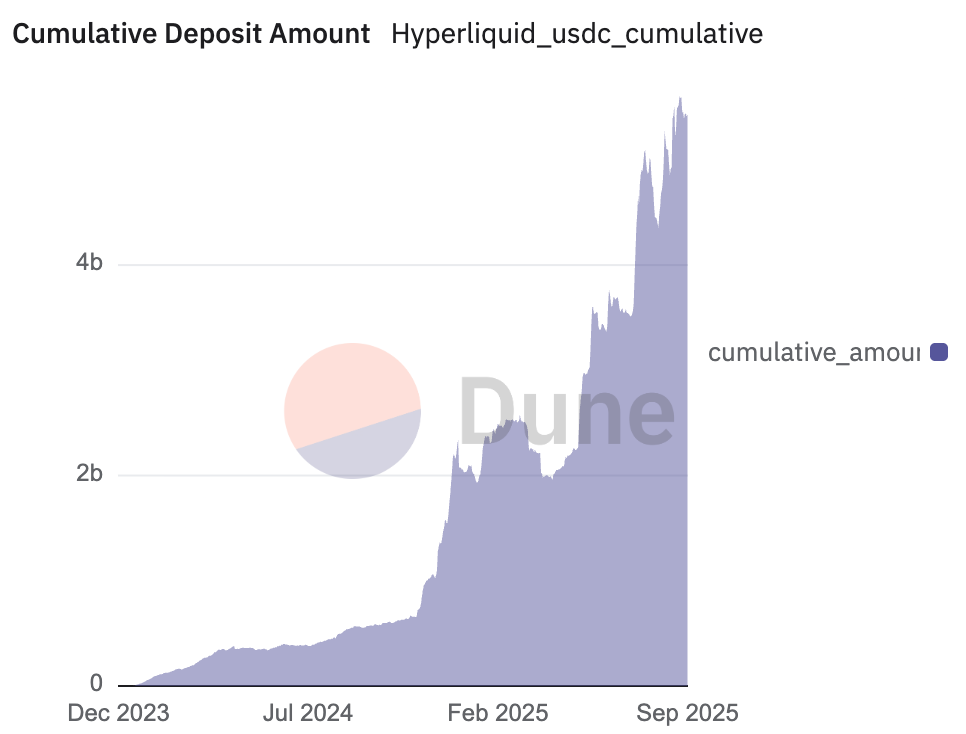

В Hyperliquid — одной из самых быстрорастущих perp-площадок DeFi — заблокирован многомиллиардный приз. Благодаря выдающемуся пользовательскому опыту и стремительному росту аудитории, платформа стала ведущей площадкой для деривативов на блокчейне: её торговый движок питается более чем 5,6 млрд долларов в стейблкоинах, почти все — это USDC от Circle.

Этот капитал обеспечивает значительный доход от резервов, который сейчас уходит внешним структурам. Сообщество Hyperliquid решило вернуть эти финансовые потоки в экосистему.

14 сентября состоится ключевое голосование Hyperliquid. Валидаторы сети определят, кто получит контроль над USDH — первым нативным стейблкоином платформы. На кону не просто токен — а контроль над финансовым механизмом, способным вернуть в экосистему сотни миллионов долларов. Всё проходит прозрачно, в ончейне — это аукцион госдолга или миллиардный запрос котировок нового поколения, где валидаторы (стейкеры HYPE) принимают решения: кому чеканить USDH и как перераспределять доход на миллиарды долларов.

Претенденты радикально различаются: команда криптоэнтузиастов, нацеленная на максимальное единство интересов, против институтов с миллиардами и отточенной машиной традиционных финансов.

Проверенная бизнес-модель: $220 млн ежегодно

Чтобы оценить масштаб, следуйте за капиталом. Сейчас лидирует USDC — Circle, её эмитент, получает внушительную прибыль, размещая резервы в казначейские облигации США: $658 млн за квартал. Hyperliquid планирует реализовать ровно эту стратегию.

Заменив сторонние стейблкоины на собственный USDH, сеть перестанет отдавать доходность вовне и будет накапливать её внутри. Уже при текущих резервах USDH может приносить до $220 млн в год. Это превращает Hyperliquid из арендатора в собственника — платформа сама создаёт ликвидность и базу для роста. Для Circle это серьёзный вызов: потеря резервов Hyperliquid может сразу сократить выручку на 10%, показав, как много компания зарабатывает на процентах.

Вопрос не в самой цели, а в том, кому доверить её реализацию.

Circle не отступает. Ещё до объявления о запуске USDH эмитент USDC начал укрепляться на Hyperliquid, анонсировав в июле запуск native USDC и CCTP V2. Решение обеспечивает мгновенные переводы USDC между цепочками — без токенов-обёрток и устаревших бриджей. Circle подключает институциональные on-/off-ramp через Circle Mint. Ясный сигнал рынку: публичный эмитент USDC не отдаст ликвидность Hyperliquid конкуренту без борьбы.

Претенденты: столкновение стратегий

Для USDH предложено несколько альтернативных моделей — каждая задаёт уникальный курс развития Hyperliquid.

Команда Native Markets — внутренний проект Hyperliquid — одной из первых после анонса объявила о планах создать GENIUS Act–совместимый стейблкоин специально для платформы. В проект заложены фиатные шлюзы для ввода-вывода и участие фонда поддержки Hyperliquid в распределении прибыли. В составе — опытные лидеры вроде MC Lader, экс-президента Uniswap Labs, хотя часть сообщества сомневается в сроках и финансировании заявки. Это локальная команда с акцентом на комплаенс, ончейн-экспертизу и возврат ценности в экосистему. Преимущество — проверенный проект с высокой регуляторной устойчивостью и тесной связью с $HYPE; недостаток — тревоги о сроках и масштабах реализации.

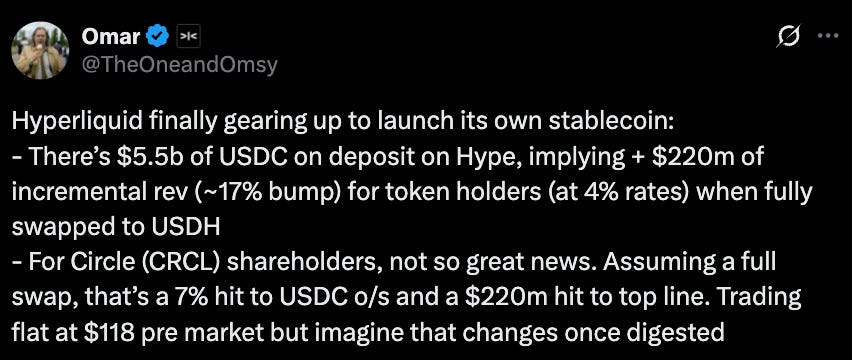

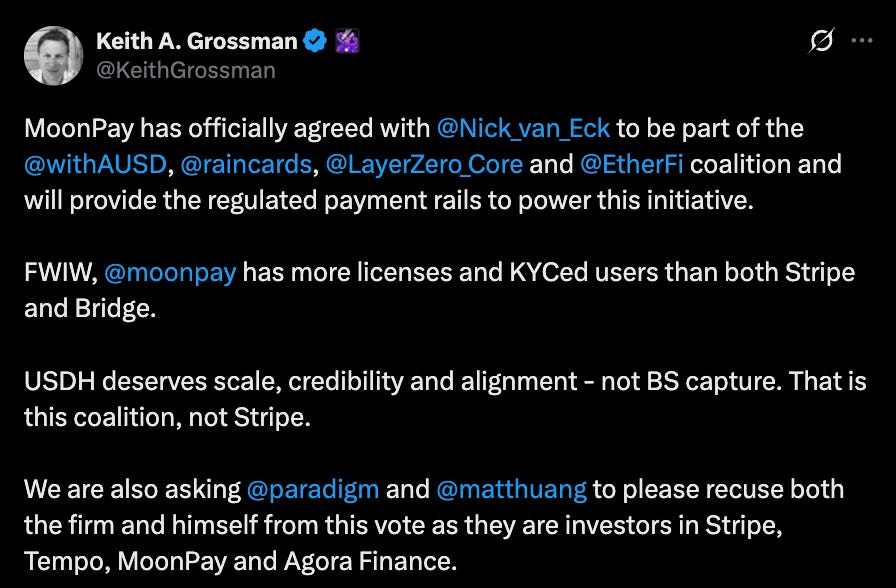

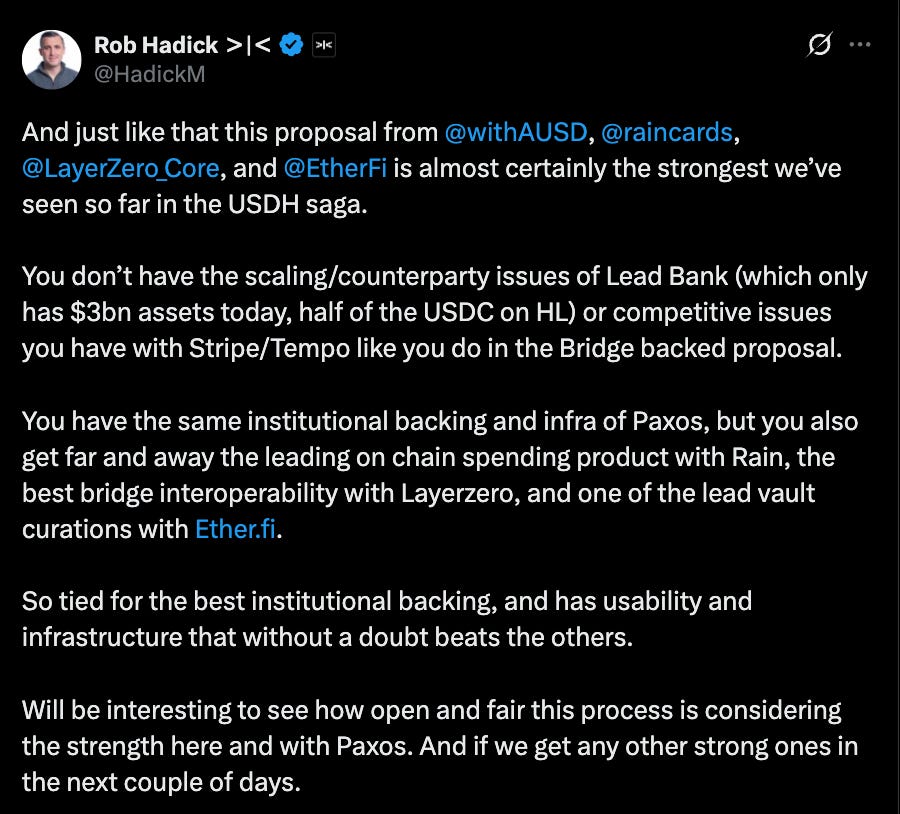

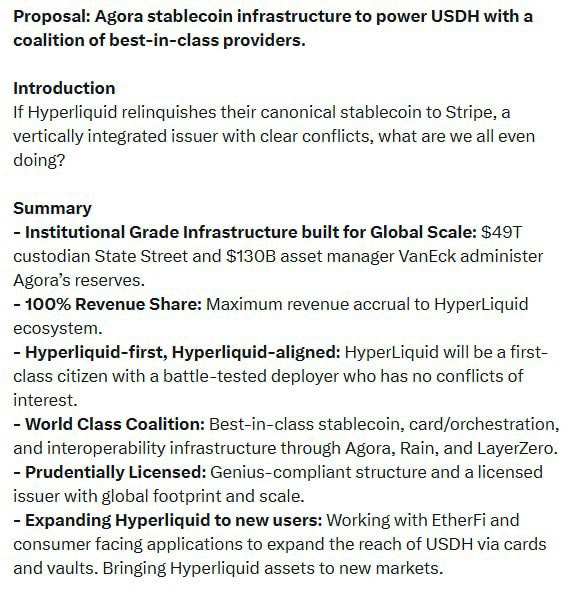

Активнее всех продвигает предложение Agora — поставщик инфраструктуры для стейблкоинов, собравший пул партнёров. Среди них — MoonPay (криптоввод с широкой лицензией и KYC-базой, превосходящей Stripe);

Rain — для мгновенных ончейн-платежей и карт, LayerZero — для топового кроссчейн-функционала.

Agora только что привлекла $50 млн инвестиций во главе с Paradigm и делает акцент на комплаенсе (аудите резервов). Её резервы размещаются в State Street и управляются VanEck, а аудитирует Chaos Labs. Минимум $10 млн ликвидности будет предоставлено через Cross River и Customers Bank. Институциональный проект с ключевым принципом: весь чистый доход с резервов USDH направляется в экосистему Hyperliquid. Это означает: рост стейблкоина напрямую увеличит доход держателей HYPE. Сильные стороны — институциональный уровень, масштаб и капитал. Риски — зависимость от банков и кастодианов, которые вводят оффчейн-узкие места, что противоречит дефи-природе USDH.

Stripe (после покупки Bridge за $1,1 млрд) предложила превратить USDH в опору глобальной сети стейблкоин-платежей. Bridge уже позволяет принимать стейблкоин-платежи (USDC и др.) более чем в 100 странах с минимальными комиссиями и мгновенным расчётом, а интеграция в Stripe даёт ему регуляторную устойчивость, мощный API и оплату картами. Компания запускает собственный фиатный стейблкоин USDB в Bridge — для снижения внешних расходов и защиты оборота. Ключевая выгода в масштабе и бренде Stripe, который может вывести USDH в массовые расчёты. Риск — стратегический захват: если вертикально интегрированный финтех с собственной сетью (Tempo) и кошельком (Privy) получит контроль над ключевым денежным слоем Hyperliquid.

У других претендентов — свой курс. Paxos (регулируемый нью-йоркский траст) — самый консервативный вариант: приоритет — комплаенс. Компания обязуется 95% дохода направлять на обратные выкупы HYPE и листить HYPE в PayPal, Venmo, MercadoLibre. Такой институциональный охват не обещает ни один из конкурентов. Даже при смягчении регулирования в США при Трампе, Paxos — выбор тех, кто ставит на долгосрочную устойчивость и прозрачность. Риски — полная зависимость от фиата и банков, уязвимость к регуляторным потрясениям (такой же фактор привёл к краху BUSD).

Frax Finance — DeFi-нативный контраст. Эта команда выросла из криптоэкосистемы и делает ставку на ончейн-дизайн, глубокое децентрализованное управление и схему распределения доходности, которая близка криптоэнтузиастам. В их модели USDH обеспечивается 1:1 за счёт frxUSD и облигаций с управлением топовых управляющих (BlackRock), с мгновенным выводом в USDC, USDT, frxUSD и фиат. 100% доходности от резервов направляется пользователям Hyperliquid, а управление полностью валидаторское. Преимущество — проверенная, доходная модель, управляемая сообществом. Недостаток — двойная зависимость: frxUSD и фиатные облигации, что может снизить адаптацию по сравнению с фиатными аналогами.

Konelia — малозаметный кандидат, подавший заявку через тот же ончейн-аукцион. В её предложении акцент на комплаенсе, управлении резервами и интеграции с инфраструктурой Hyperliquid L1. Однако подробностей мало, а интерес сообщества ограничен — поэтому шансы Konelia минимальны на фоне сильных соперников.

xDFi — команда DeFi-ветеранов из SushiSwap и LayerZero — предлагает выпустить полностью криптообеспеченный омничейн-стейблкоин USDH на 23 EVM-цепях с первого дня. В обеспечение идут ETH, BTC, USDC, AVAX, а балансы синхронизируются между сетями на xD без бриджей и фрагментации. По токеномике 69% дохода поступает в управление $HYPE, 30% — валидаторам, 1% — на поддержку протокола. Это полностью децентрализованный, нечувствительный к банкам дизайн, который усиливает статус Hyperliquid как хаба ликвидности. Главный риск — зависимость от волатильной криптообеспеченности и отсутствие регуляторного "зонтика" для массового внедрения.

Curve предлагает иной путь — не конкуренцию, а партнёрство. На базе механизма crvUSD LLAMMA — модель с двумя стейблкоинами: регулируемый USDH (через Paxos или Agora) и децентрализованный dUSDH, обеспеченный HYPE и HLP, размещённый на CDP Curve и управляемый Hyperliquid. Это открывает новые стратегии зацикливания, кредитного плеча и доходности, формируя маховик ценности HYPE/HLP. Curve подчёркивает стабильность и устойчивость crvUSD к волатильности и отмечает, что его CDP-модель уже приносит от $2,5 до 10 млн долларов в год при объёме $100 млн. Сильная сторона — сбалансированное решение: комплаенс плюс DeFi-натив. Риски — размывание ликвидности и бренда между тикерами, а также риск использования собственных активов Hyperliquid как обеспечения.

Децентрализованное решение

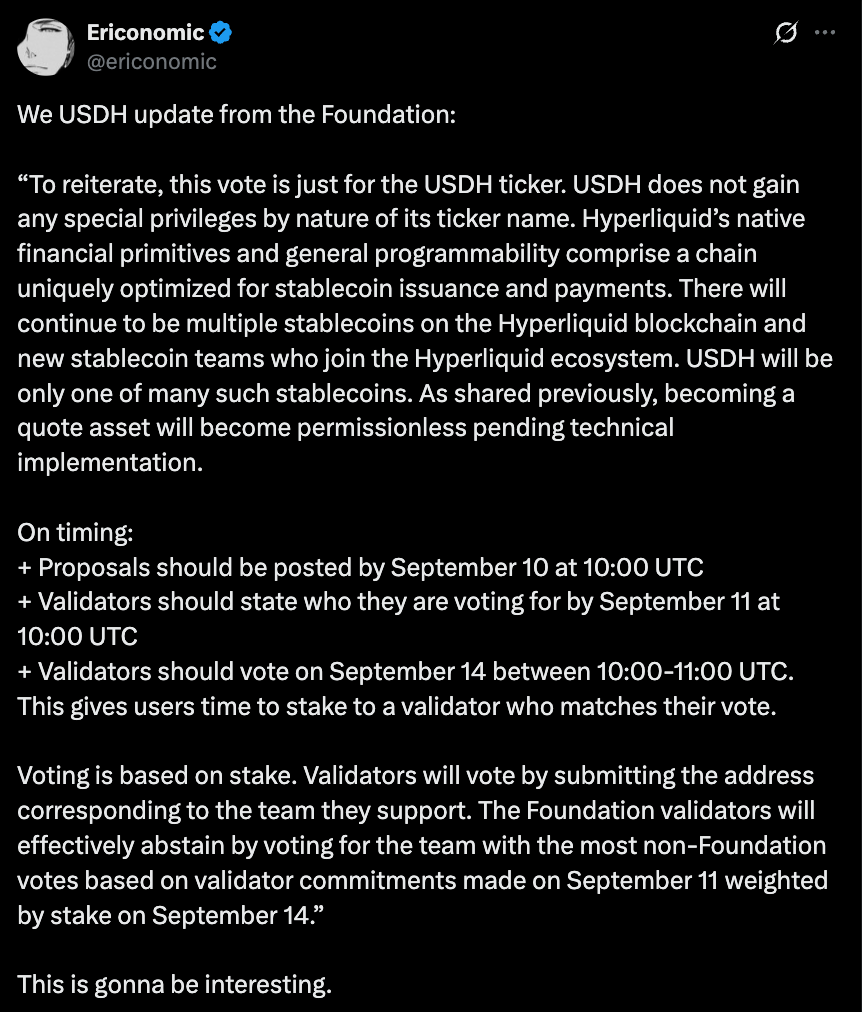

Окончательный выбор останется за валидаторами Hyperliquid в ончейн-голосовании. Чтобы гарантировать прозрачность, Hyperliquid Foundation публично отказался от участия в голосовании.

Фонд заявляет, что просто поддержит решение большинства — полностью снимая вопросы централизации и подтверждая, что власть действительно у держателей токенов.

14 сентября — это не просто дата голосования, а тест зрелости управления DeFi: сообщество впервые распределяет миллиардные контракты голосованием, а не дискуссиями о комиссиях.

Дисклеймер:

- Статья перепечатана с ресурса [Tristero Research]. Все права принадлежат оригинальному автору [@tristero">Tristero Research]. При возникновении возражений по перепечатке обращайтесь в Gate Learn — вопрос будет оперативно решён.

- Дисклеймер: мнения и выводы в статье принадлежат исключительно автору и не являются инвестиционной рекомендацией.

- Перевод на другие языки выполнен командой Gate Learn. Без прямого разрешения копирование, распространение или плагиат перевода запрещены.